High Times Ahead: A Case for the North American Cannabis Industry

With Canada’s nascent cannabis industry in its fourth year of legal operations, there is much to look forward to. When considered alongside the strong potential for federal legalization in the U.S., North America is in the early stages of a cannabis boom that will bring the industry to the forefront of the minds of investors and consumers alike.

Cannabis’ path towards North American legalization has been and continues to be an uphill climb. North America was introduced to recreational marijuana at the turn of the 20th century when Mexican immigrants brought the practice to the U.S. Shortly thereafter, prohibitory legislation was enacted in both Canada and the U.S. that criminalized the use of cannabis. In the decades following, the popularity of cannabis grew, and the use of the illicit substance exploded in the 1960s. Despite mounting calls for decriminalization, the U.S. doubled down on their anti-cannabis stance with the Controlled Substances Act of 1970 which defined cannabis as a Schedule I drug (other Schedule I drugs include meth and heroin) – a designation that shockingly persists to this day.

Late in the 20th century, cannabis’ reputation began to change with widespread acknowledgement of its medical benefits. California was the first state to legalize medical marijuana in 1996, and in 2000, the Ontario Court of Appeal ruled that cannabis must be made available for medical uses. The election of Prime Minister Trudeau in 2015 then accelerated Canadian cannabis legalization with federal legalization occurring in October 2018.

South of the border, where cannabis is still federally illegal, 18 states (19, including Washington D.C.) have legalized the substance recreationally and an additional 18 have legalized it for medical use only.

Source: DISA

In terms of national sentiment, a recent Gallup poll pegged support for U.S. federal legalization at 68%. Although support is much more pronounced amongst Democrats, 50% of Republicans surveyed also agree with legalization, making a bipartisan legalization effort a viable path for the future.

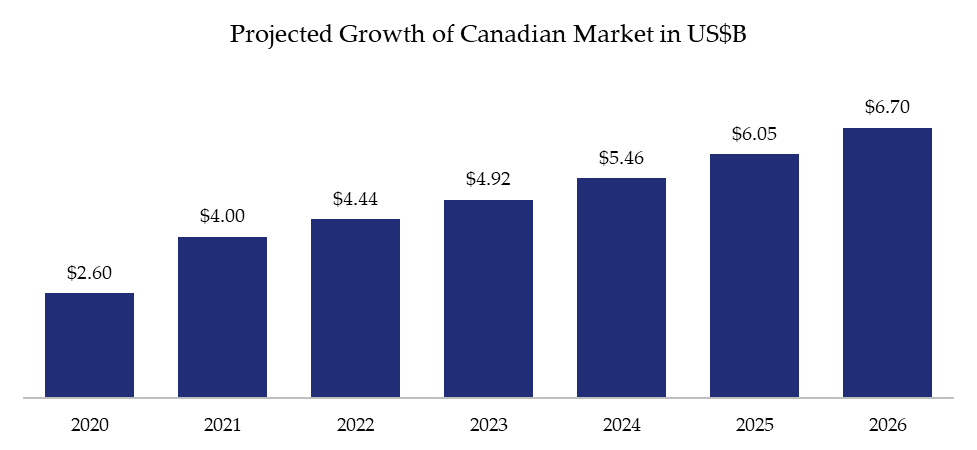

The Canadian Market

Since the Cannabis Act passed the House of Commons in late 2017, the journey of the Canadian cannabis industry has been turbulent. Upon legalization, investors and industry players rushed to gain the first-mover advantage in a blue ocean market. Capital markets also experienced a flurry of activity, as cannabis companies cashed in on the excitement that lifted share prices and drove down their cost of capital. However, in the years that followed, investor sentiment began to falter, illustrated by the value of shares in one of Canada’s biggest cannabis players, Canopy Growth, falling ~80% since federal legalization.

So, what could have caused such a decline?

Over-restrictive regulation and easily accessible illicit markets paired with unrealistic expectations for consumer demand gave way to early, market-wide volatility. The pandemic and its related challenges have only exacerbated the problem, resulting in the industry’s depressed stock prices today.

Source: Gallup

Historical prices from October 2nd, 2017, to March 2nd, 2022 | Source: Yahoo Finance

Although the Canadian cannabis bubble has popped, there are many factors that point to a positive future for the industry. In fact, projections for Canadian cannabis sales see the market growing at a compounded annual growth rate of 11% from 2021 to reach a value of $6.7 billion USD by 2026.

Source: BDSA

Underpinning this growth is the transition of cannabis users from the illicit market to the legal adult-use market. In terms of total expenditure, the legal market has already surpassed the black market with Ontario, the province with the highest market share (~39%), reaching this threshold earlier in 2021.

Another factor helping to facilitate the transition of users to the legal market is a boom in the number of dispensaries opening, which increases accessibility and convenience for consumers. Though the pace of retail store openings post-legalization was sluggish, looser regulatory policies have helped to push the national store count above 2,600, with over 1,000 of those stores being located in Ontario.

On the basis of market capitalization, some of the largest licensed producers (“LPs”) in Canadian cannabis include Canopy Growth Corp. (TSX: WEED), Tilray Brands (TSX: TLRY), and Aurora Cannabis (TSX: ACB), with many other smaller players growing rapidly. These companies are vertically integrated, meaning they are concerned with the production, distribution, and sale of cannabis and cannabis-related products.

Regarding Canadian M&A, the past few years have seen some exciting business combinations that will undoubtedly impact the future of Canadian cannabis. For example, in late 2020, Tilray and Aphria announced a merger that would make the combined entity the largest global cannabis company in the world based on Pro-forma revenue.

While the Canadian market presents an attractive opportunity in itself, LPs have been proactive in positioning themselves to capture a share of the more lucrative U.S. market upon federal legalization. To accomplish this, firms have pursued alternative transaction structures, such as purchasing an option to acquire U.S. operators, acquiring the debt of U.S. cannabis companies, and purchasing CBD companies that don’t face the same regulatory burden as “plant-touching” companies.

The U.S. Market

The U.S. cannabis industry appears to be entering a new phase brought on by widespread state legalizations. Indeed, the 2020 election ushered in a much larger addressable market with down-ballot legalization votes garnering majority support in multiple states. The trend of state legalization continued in 2021 with states like New York and Virginia legalizing recreational cannabis, adding momentum to the growth of the industry. In fact, after generating an estimated US$18B in sales in 2020, the industry is projected to grow to ~US$48B by 2026, representing ~75% of the global market share.

Source: Ontario Cannabis Store

Despite strong future prospects, a complex regulatory environment has created numerous operational difficulties for American cannabis firms and has undoubtedly stunted the growth of the industry as a whole. For example, cannabis’ illegality at a federal level means interstate commerce is still prohibited. Multi-state operators (“MSOs”) residing in multiple jurisdictions are then forced to vertically integrate at a state level, adding to the complexity and cost of their projects.

An additional problematic layer to the federal ban is the access, or lack thereof, that cannabis companies have to domestic capital markets. U.S. cannabis companies are not allowed to list on U.S. exchanges like the New York Stock Exchange and the NASDAQ due to the substance’s illegality. This has led companies to pursue listings on Canadian exchanges like the Canadian Securities Exchange for crucial access to capital. Moreover, due to cannabis’ Schedule I status, financial institutions are subject to punitive actions from federal regulators for working with American cannabis companies, even if they are legally operating according to state law.

In response to changing societal opinions on cannabis and effective lobbying, there are pieces of legislation currently working their way through Congress that, if passed, would alleviate regulatory burdens, and serve as a catalyst for the industry. One of the more popular legislative proposals is the Republican-led States Reform Act. While being less progressive than the Democrat-proposed Cannabis Administration and Opportunity Act and Marijuana Opportunity Reinvestment and Expungement (“MORE”) Act, the States Reform Act still includes provisions that would strengthen the U.S. cannabis industry. The bill removes cannabis as a federal Schedule I controlled substance and empowers states to regulate cannabis at their discretion, in addition to guaranteeing the release and expungement of those convicted of federal cannabis crimes. The States Reform Act would also allow financial institutions to work with cannabis companies, effectively solving the issues that the another popular piece of legislation, the Safe and Fair Enforcement (“SAFE”) Banking Act, is concerned with. Further, interstate commerce between legalized states would be allowed, resulting in the creation of new markets for cannabis firms to enter.

Regarding industry composition, some of the biggest MSOs include Trulieve (CSE: TRUL), Curaleaf (CSE: CURA), and Green Thumb Industries (CSE: GTII). From a financial point of view, these companies have performed much better than their Canadian counterparts in terms of both sales and profitability. In fact, the average gross margin generated by some of the biggest MSOs is ~56% compared with an average LP gross margin of ~8%.

Like the Canadian market, U.S. M&A activity also picked up in 2021 and is showing no signs of stopping soon. Some of the landmark deals of the past year include Trulieve’s acquisition of Harvest Health & Recreation and Verano's acquisition of Goodness Growth. Contributing to this acceleration in deal-making is the introduction of new legal markets, which has placed competitive pressure on firms to grow their national market share.

Evidently, both the Canadian and American cannabis markets show strong promise for the future. One can expect the next few years to be filled with impactful regulatory changes and a surge of capital markets activity – all of which will shape the North American cannabis industry for years to come. While obstacles lie ahead with navigating complex regulatory frameworks and a highly partisan U.S. Congress, it certainly is an exciting time for a young and dynamic industry.