The Great Wealth Transfer Is Here but Is the Next Generation Ready?

Imagine inheriting a fortune overnight but lacking the knowledge to manage it – a task both exciting and nerve-racking. This is the reality facing many young adults, with an unprecedented $84 trillion in assets set to change hands over the next 20 years, according to estimates by the consulting firm Cerulli Associates. Complicating factors such as a gap in financial literacy, changing priorities in asset allocation, and a lack of estate planning highlight the challenges associated with this monumental shift of wealth. Nonetheless, proactiveness is key for families to effectively navigate the transition and make the Great Wealth Transfer a little less daunting.

Understanding The Great Wealth Transfer

The scale of this so-called “Great Wealth Transfer” is truly staggering. Prior to taking a deep dive into why this generational event is so important and how families can appropriately prepare, it is essential to analyze where the money is coming from and where it is going based off of different generation groups, net worth classes, and geographies.

Of the $84 trillion in assets to be inherited over the next 20 years, the vast majority of these assets – around $72 trillion – is projected to be inherited by younger generations, while the remaining portion will be allocated to charitable causes. On the receiving end of the inheritance, Gen X is the most common beneficiary, inheriting a total of $30 trillion through 2045, followed by Millennials, slightly behind at $27 trillion, as demonstrated in Figure 1.

Figure 1: Estimated Inherited Wealth Through 2045 ($T) By Generation (Merrill Lynch, 2024)

Alternatively, another interesting angle to analyze the Great Wealth Transfer is in terms of net worth tiers and how concentrated the transfer is among UHNWI (ultra-high net worth individuals). Specifically, as the exhibits below demonstrate, there is a disproportionate amount of the wealth transfer coming from the top echelon, with ~16% of the total wealth passed on coming from less than 1% of all individuals (the $1B+ net worth tier) (Figure 2 and 3).

Figures 2 and 3: Analyzing The Great Wealth Transfer By Net Worth Tiers (Altrata, 2024)

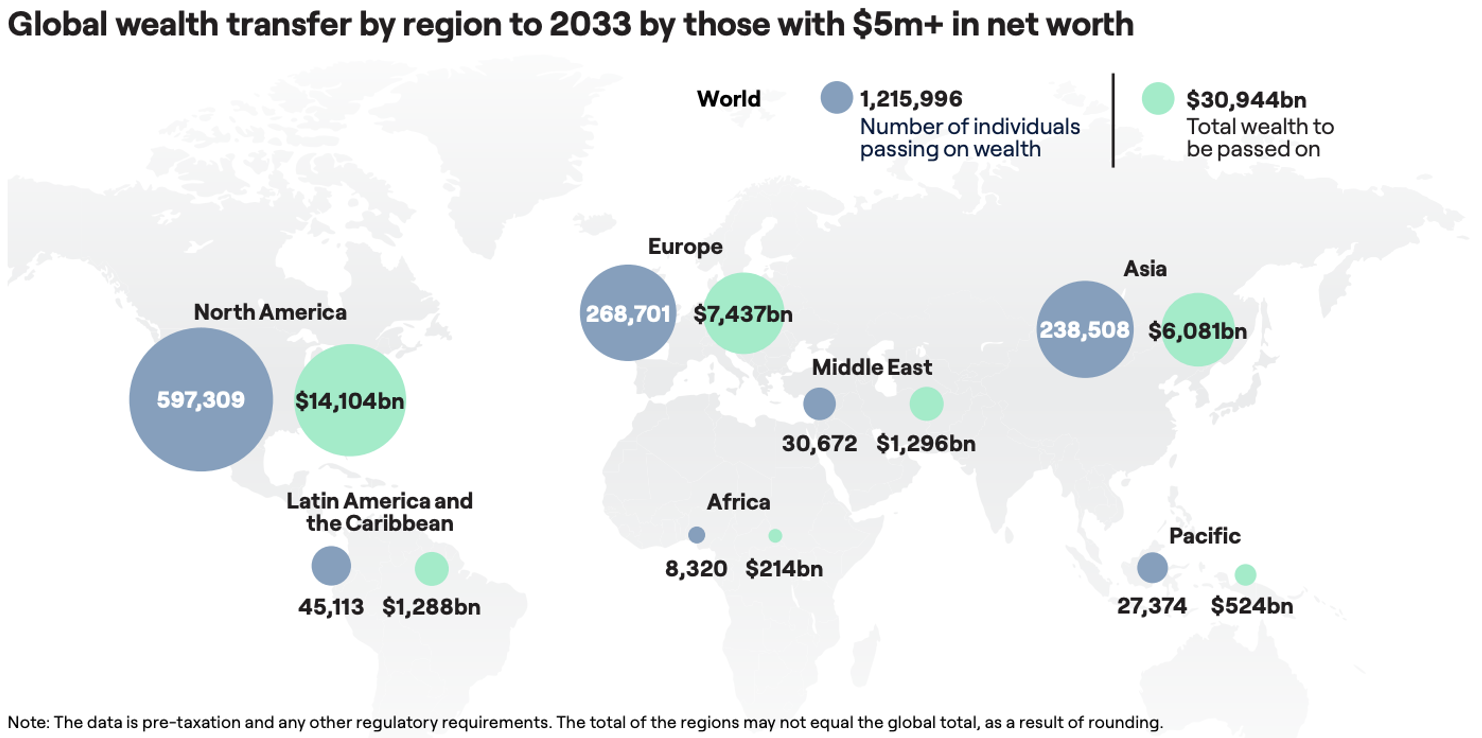

Another notable insight into how the Great Wealth Transfer is evolving is on a geographic basis. As one might expect, the majority of the wealth transfer, both in terms of the value of wealth as well as number of individuals passing on wealth, is occurring in North America. As illustrated in Figure 4, Europe and Asia are a distant 2nd and 3rd respectively, with various other regions across the globe also contributing to this monumental shift in wealth.

Figure 4: Global Wealth Transfer by Region to 2033 by Those With $5M+ in Net Worth (Altrata, 2024)

What Could Go Wrong?

Though the Great Wealth Transfer should provide future heirs with an abundance of excitement, families currently face significant challenges in managing the impending wealth transfer which can complicate the inheritance. Specifically, there is an alarmingly high proportion of the population that is financially illiterate. As one can imagine, the potential issues that may arise with such individuals inheriting large sums of money can be disastrous. Moreover, young generations (i.e. the beneficiaries of the Great Wealth Transfer) have drastically different investment preferences compared to their predecessors, which may lead to a variety of intergenerational complications in terms of what assets the money is being put towards.

Lack of Financial Literacy

Research from RBC Wealth Management also indicates that more than one-third of American adults today say that no one taught them about investing. Among the different generations, baby boomers are the least likely to have had any sort of financial instructions, with the proportion at a whopping 38% for this group. Despite this concerning dynamic, a beacon of hope emerges in the fact that the vast majority of Americans today – 87% in fact – believe that financial literacy is so crucial that it should be taught to kids in school, emphasizing the growing awareness surrounding the topic. Experts also stress the importance of early financial education, suggesting that it's never too soon to start. Teaching children about money through allowances or compensation for household chores will help them understand the responsibilities and benefits of financial management. Beginning this education process when children are younger allows parents to exercise control over the learning environment, potentially preventing more severe financial mistakes later in life.

Changing Investment Preferences and Priorities

In addition to changes in the approach to financial advisory, younger generations have a variety of unique priorities in terms of what they invest in. Specifically, the traditional 60/40 stock and bond investment portfolio garners much less appeal from young investors; rather, the next generation is far more inclined to seek out alternative investments. Young investors that have at least $3M in investable assets allocate nearly one-third of their portfolio toward alternative investments, including hedge funds, private equity, crypto, and digital assets. At the same time, less than half of the portfolio for these young investors is held in traditional stocks and bonds. This point is strengthened by a Bank of America survey that suggested that 75% of investors aged 21-43 believe it is not possible to achieve “above-average returns” solely with traditional stocks and bonds, whereas only 32% of investors 44 years of age and older believe this to be the case. ESG investing is also a hot topic among the next generation, with 73% of those ages 21-43 currently owning sustainable investments in their portfolio, compared to only 26% for all survey respondents.

The wide discrepancies are further shown in the figures below, comparing what younger investors and older investors believe to be the greatest investment opportunities for growth (Figure 5). One noteworthy constant is investors’ affinity towards real estate. Younger individuals currently face steep barriers to entering the real estate market, with elevated interest rates and supply challenges; however, the Great Wealth Transfer should enable more of them to become first-time homeowners – or even purchase a secondary residence – either through inherited property or liquid assets.

Figure 5: Investors’ Most Favoured Asset Classes For Growth (Bank of America, 2024)

When Does The Next Generation Start To Get Exposed In Family Wealth Decisions?

Of note as well is the underrepresentation of younger generations by financial advisors. Though Millennials and Gen Z represent over 42% of the U.S. population, they account for only 14% of financial advisory clients, demonstrating a strong disconnect. Despite the current disconnect, 65% of Millennial and Gen Z investors believe that a financial advisor is important to achieve financial success, compared to just 56% of baby boomers. The question becomes: how do younger generations naturally get involved with family wealth, including being introduced to financial advisors? Figure 6 suggests that it’s most common for those aged 26-35 to be involved in decisions about family wealth and introduced to the advisors of the family. No matter what age the next generation is exposed to regarding the intricacies of family wealth, it is critical that this involvement is not delayed indefinitely as the later families approach these issues, the more potential complications may emerge.

Figure 6: Progression of Involvement With Family Finances by Age (Julius Baer, 2023)

Strategies For Families To Navigate The Great Wealth Transfer

If there is one word to describe the Great Wealth Transfer, that word would be uncertainty. Between changing investment preferences, a lack of formal financial education, and the overall daunting nature of more than $80 trillion being passed down in the next 20 years, there will no doubt be challenges ahead – both for individual families as well as the broader economy. On a micro level, each family must take the appropriate steps to mitigate these uncertainties and ensure a transition of wealth that is as seamless as possible. If this is accomplished on an individual family-by-family basis, the macro challenge of dealing with the entire Great Wealth Transfer will be less intimidating.

Estate planning is the first essential step that all individuals must take to protect their wealth and ensure appropriate transfer of assets upon death; yet, a shocking 68% of Americans do not have a will, a 6% increase year-over-year since 2023. If you die without a will – also known as intestate – the consequences depend on where an individual resides and specific laws by jurisdiction. In Ontario, for example, when a person dies intestate, Ontario's Succession Law Reform Act sets out how the estate is to be distributed. In such cases, the people who can inherit the estate of the deceased include their spouse and closest next-of-kin, barring some exceptions. There is a myriad of additional legal considerations that can cause a variety of complications and, as an aside, also lead to substantial legal fees. In turn, crafting a will is a critical decision every individual should make to proactively approach inheritance, ensuring that the transfer of assets is approached in a way that is most appropriate.

Though the causes of stress and strain within families are different depending on the generation, interpersonal family dynamics are the one of the leading causes of complications (Figure 7). This dynamic serves to highlight the fact that the Great Wealth Transfer is not solely a financial issue of monetary assets; rather, consideration for the emotional and sentimental elements of inheritance are equally if not more important. As Leanne Kaufman, president and CEO of RBC Royal Trust, notes: “money, and for that matter many assets, come with some emotional attachments… it is very difficult to remove emotion from pretty much every aspect of our lives.” Given these challenging factors, both financial and emotional, it is highly recommended that families seek out counsel from professionals in the industry. Estate planning lawyers as well as other trusted advisors have immense experience with the subject and can offer invaluable, tailored solutions for families to navigate the nuances of inheritance and wealth transfer effectively. The issue of estate planning is one where families do not want to “cheap out” by not hiring an advisor.

Figure 7: Reasons For Inheritance-Related Strain Within Families (Bank of America, 2024)

Ultimately, the Great Wealth Transfer is no doubt an issue that is of critical importance to families worldwide and one that may seem quite daunting to the next generation. To navigate the inherit complexities of this transition successfully, early financial education and open intergenerational conversations are essential. Additionally, working with trusted advisors can help bridge the knowledge gap and ensure responsible estate planning. When faced with uncertainty, the ultimate key to success is proactiveness. If the appropriate steps are taken by families to ensure a seamless transition to the next generation, the Great Wealth Transfer can become a pivotal event that pushes the world economy ahead as opposed to holding it back in the past. It is up to the current generation to take the right actions today in order for future generations to reap the rewards.